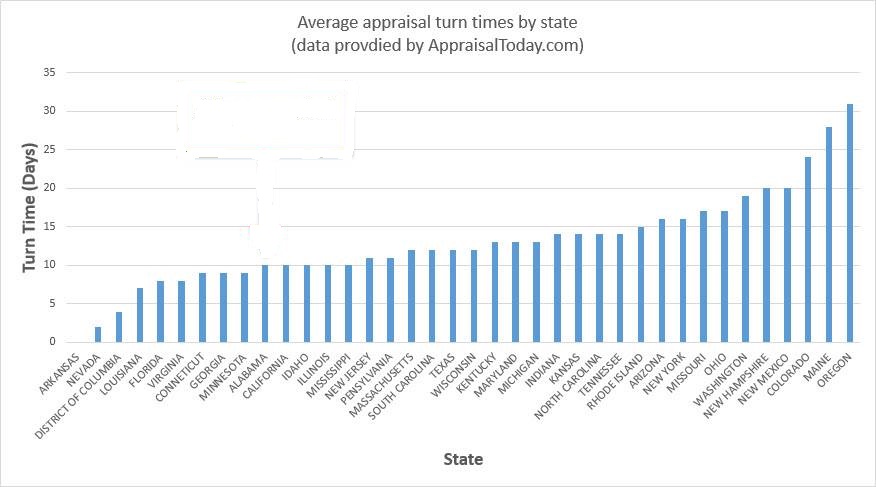

Potentially compounding an appraisal issue based on value and/or conditions is the wait…Oregon is ranked 50th in regard to appraisal turn time. In a market with as little inventory as we currently have, waiting 30 + days for an appraisal turn can make a once highly sought-after listing old news.  There certainly are enough considerations from the buyer’s qualifications coming into question during a transaction to issues related to appraisals that would make any rational seller seek out the easiest path to the closing table. What about those sellers who don’t necessarily consider being separated from those issues to be ‘priceless’? Would sellers entertain the possibility of accepting a financed offer over cash, if the price were right? It all depends on a seller’s comfort level with their knowledge of how financed offers work. In most cases that knowledge is going to come in a crash course from their Broker as it may be the first transaction the seller has dealt with recently, or ever. Most likely, the difference between cash & financed offers isn’t something a seller will have considered until the very moment it’s presented to them.

There certainly are enough considerations from the buyer’s qualifications coming into question during a transaction to issues related to appraisals that would make any rational seller seek out the easiest path to the closing table. What about those sellers who don’t necessarily consider being separated from those issues to be ‘priceless’? Would sellers entertain the possibility of accepting a financed offer over cash, if the price were right? It all depends on a seller’s comfort level with their knowledge of how financed offers work. In most cases that knowledge is going to come in a crash course from their Broker as it may be the first transaction the seller has dealt with recently, or ever. Most likely, the difference between cash & financed offers isn’t something a seller will have considered until the very moment it’s presented to them.

What due diligence should a listing Broker employ when analyzing a buyer’s offer with a seller? Regardless of whether it’s to make a determination about weighing the merits of financed versus cash, it should be standard practice to contact the lender directly to get as much insight about the buyer & lender as both. Unfortunately, the percentage of listing Brokers who contacts the buyer’s lender directly in order to verify information already stated on a Pre-approval letter, or gather additional insight about the buyer, is a mere fraction of what it should be. I would venture to say that when I’m representing a buyer whose offer is being seriously considered that our lender is contacted by the listing Broker less than 10% of the time. That may in part be due to my making a good case for my buyer clients & the listing Broker feeling all the issues have been satisfactorily addressed but, there are always pieces to the puzzle that can only be solved with the lender’s input.

Having a pre-approval in hand gives us a head start in dissecting the appraisal process and possibly putting to rest some of the concerns that might cause a seller to dismiss a financed offer in lieu of cash. Knowing the difference between Mortgage Brokers, Mortgage Bankers & Commercial lenders will be the very first consideration for the seller to take into account when presented with a financed offer. This not only gives the listing Broker the opportunity to educate the seller on differences that can truly separate one from the other but, it also should be the first subject to the table with the lender. Commercial lenders, or the big Banks that You and I may have our checking and savings accounts with, are required to use an appraiser from the Statewide pool on a first come first serve basis. In Oregon, we’re just shy of 1,500 appraisers Statewide thus, the first challenge is hopefully getting someone who is somewhat familiar with the neighborhood in which they are being asked to make a value judgment. Secondarily, the sheer volume of appraisals being ordered by large commercial banks creates a backlog that is compounded by an antiquated compensation system that many times hinders the capabilities of those appraisers in making adjustments when the value has come into question. Appraisers are exceedingly well-educated in their field thus, the vast majority of challenges they face are due to regulatory & industry demands that simply haven’t kept pace with the times. On the flip side of the coin are Mortgage brokers & bankers who may work under local Company names you’re familiar with, some being rooted here in Oregon while others have a National presence. This would be the opportunity for a listing Broker to inquire as to the working relationship the lender has with its much smaller pool of appraisers. Better yet, would be to leave open the opportunity for that lender to boast about the excellent relationship they have with their appraisers and the quick turns they are accustomed to. Obviously, the lender feeling a sense of pride in their working relationship with their appraisal pool and offering evidence of results without being prompted to do so may go a long way toward a more favorable view of a financed offer. Of course, this requires the listing Broker to exercise due diligence on behalf of their seller clients above & beyond the listing and marketing of their property that resulted in a multiple offer scenario. Utilizing Social Media to gain optimal exposure, as well as marketing to cooperating Brokers via Maximizing Multiple Listings are critical components to getting a seller to a position where multiple offers are a factor. The value derived from those first two steps is unfortunately the final ‘resting place’ for some listing Brokers who may feel their duties to the seller have been satisfied by having multiple offers on the table. It’s at this point that a Broker truly can determine his or her own value to the seller by providing Negotiation insights that outline options and considerations far above & beyond simply being presented with an offer(s) and directed to the location on the first page that states the offered sales price.

In order to provide a seller with as much pertinent information to make an informed decision, be it which offer to accept or whether a financed offer should be given more weight in comparison to cash, it’s important to know something about the makeup of that particular buyer. In addition, creating a scenario of some common traits that cash buyers sometimes exhibit can be helpful to a seller. As was mentioned earlier, buyers with cash resources do have certain expectations that go along with their offers. In addition to the knowledge that their offer has a greater likelihood of being accepted there is also a realization that their capability to close sooner & avoid financing issues is looked upon favorably by most sellers. Each & every cash buyer places a different value on his/her ability to put to rest some of the seller’s concerns. Exercising due diligence above & beyond simply reviewing the buyer’s proof of funds statement can be a crucial part of the decision as to whether or not cash is truly king in all cases. On numerous occasions, I’ve had Buyer’s Broker’s casually stated that their cash buyers had just terminated a transaction prior to this one and it was ‘easy to do because it was cash’. In reality, it really isn’t any easier to do but, that mindset is the key component here for the seller to consider, once it’s conveyed by the listing Broker. Of course, all this wouldn’t take place if it were simply left to telling all the buyer’s Brokers to bring their ‘Highest & Best Offers’ and have no conversations above & beyond that. Unfortunately, that is all too often what takes place.

Having an understanding of how an appraiser views a home & subsequently makes a value determination is vitally important information to convey to a seller. Deciding between taking the seemingly easier road with cash versus a financed offer that may ‘net’ tens of thousands more to a seller requires serious discussion based upon revisiting comparable sales. In addition to the due diligence required to make this call, it may also bring into question the listing Broker’s original comparable sales. Unfortunately, as is all too often the practice of some Brokers to ‘shut it down once offers have been received, there may also be a reluctance to revisit comparable sales for a variety of reasons, none of which benefits the seller.

Cash certainly has its advantages however, its uses are determined by the holder of those funds, Determining what other motivations they may have for purchasing this property, whether have they purchased others with cash, whether have they been successful, etc. Creating a profile of a cash buyer can be vitally important information in helping the seller predict how they might act in a transaction.

Ultimately the choice as to whether a seller should accept a financed offer when a cash offer is also on the table has much more to do with merely a difference in price. An understanding of the market, appraisal of common practices, and an ability to ask questions to gain helpful insight about parties to the transaction are vitally important factors. With over two decades in the industry, I pride myself on having developed a knowledge base of issues and an ability to act in a beneficial way on behalf of my clients. If your looking for superior representation in your next purchase or sale I would be glad to meet with you to see how we might work together.

Bob Zawaski G.R.I.

Oregon Licensed Principal Broker

Investors Trust Realty